What Is Self-Funding?

Self-funding is one of the ways an employer can choose to offer a healthcare plan to their employees. An employer has a self-funded (or self-insured) group health plan if the employer assumes the financial risk associated with providing health care benefits to its employees. Instead of paying fixed premiums to an insurance company, the employer pays for medical claims out of pocket as they are incurred. Why would an employer choose self-funding? Check out the graphic below!

A Step-by-Step Scenario for How Self-Funded Benefits Work:

1. An employee makes an appointment with their doctor because they are sick.

2. The employee is then asked to provide their insurance card to their physician’s office personnel, which tells the doctor’s office what type of health plan they have, how it is administered and who the claim should be sent to.

3. A claim is generated and is submitted to the Plan Administrator.

4. The Plan Administrator will determine how the employee’s health benefits work and what payment is required for their doctor).

5. The Plan Administrator pays the provider based upon the plan benefits.

6. The Plan Administrator debits the employer’s bank account for the claim.

The Explanation of Benefits

After an employee’s visit with their physician, they will receive Explanation of Benefits, or EOB, from their health plan administrator. This EOB summarizes their claim, the payments they must make, the payments health plan must make, and any other payment information regarding their claim. This statement is not a bill or request for payment, it is simply informational.

What are an Employee’s Rights Under a Self-Funded Plan?

Self-funded health plans are regulated under the federal Employee Retirement

Income Security Act (ERISA), rather than state law

as insured health plans are. Federal regulations require an employer to provide

their employee with a summary description of their health plan and certain

other documents related to the plan. The employee can also request to see a copy

of the plan document that determines what benefits are available and how they

get paid.

Self-funded group health plans are also regulated by other applicable federal laws

including the:

- Health Insurance Portability and Accountability Act (HIPAA)

- Consolidated Omnibus Budget Reconciliation Act (COBRA)

- Americans with Disabilities Act (ADA)

- Pregnancy Discrimination Act

- Age Discrimination Employment Act

- Civil Rights Act

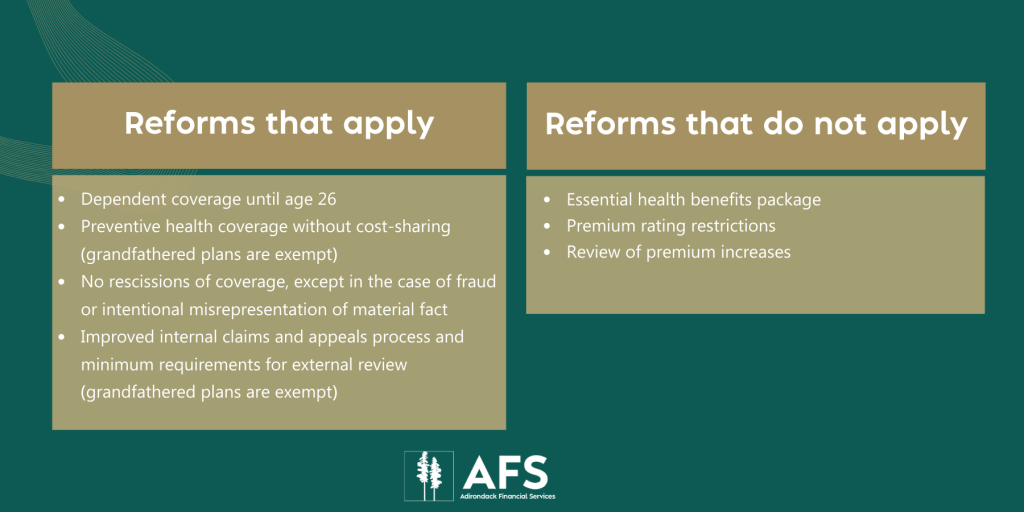

How has Health Care Reform made an impact?

Many health care reform regulations apply to all group health plans, regardless of

whether they are fully insured or self-insured, but self-insured plans are

exempt from certain provisions of health care reform. Check out the graphic

below to see examples of reforms that do and do not apply to self-insured

plans.

So, what can employees do?

Because the employer assumes the financial risk of providing an employee with health care benefits, the employer can either save or lose money depending on the level of claims incurred by their employees. Of course, employers want to be able to provide their employees with high quality health benefits, but as the cost of providing health care rises, employees too must do their part to keep benefits high and costs low.

What are some ways that employees can help save money for themselves and the company?

· Eliminate unnecessary visits to their doctor.

· Discuss healthy living and preventive care with their doctor.

· Follow prescription drug directions precisely.

· Be sure to take all their medication, even if they feel better.

· Use in-network providers if they have a Preferred Provider Organization (PPO) or Point-of-Service (POS) plan.

· Be a wise health care consumer and always ask questions if they do not understand the benefits available to them.

· Utilize Urgent Care facilities when appropriate, versus emergency rooms.

Adirondack Financial Services has expertise in transitioning organizations to self-funded health plans. Contact us for a free plan evaluation!